9 - International Trade#

9.1 - The Determinants of Trade#

The world price is the price of a good that prevails in the world market for that good.

If the world price of a good exceeds the domestic price, then the country will export that good when trade is permitted. If the world price is lower than the domestic price, then the country will import the good.

9.2 - The Winners and Losers from Trade#

When analyzing the welfare effects of trade, economists may assume that the economy of the country analyzed is small compared to the rest of the world. This assumption means that the country’s actions have a negligible effect on world markets, meaning that their tax policy will not affect the world price of goods. As such, the actors in the country are considered price takers, since they take the price of the good as determined by supply and demand.

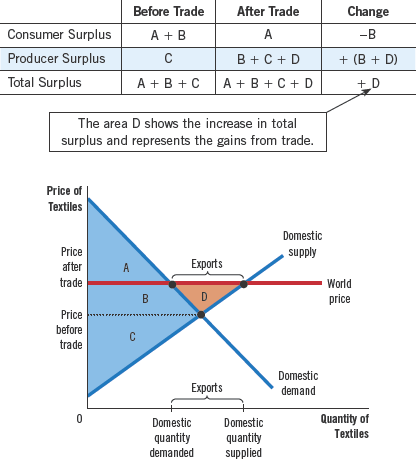

The Gains and Losses of an Exporting Country#

When trade is allowed, the domestic price changes to match the world price.

When a country allows trade and becomes an exporter of a good, domestic producers of the good are better off, and domestic consumers of the good are worse off.

Trade raises the economic level of well-being of a nation in the sense that the gains of the winners exceed the losses of the losers.

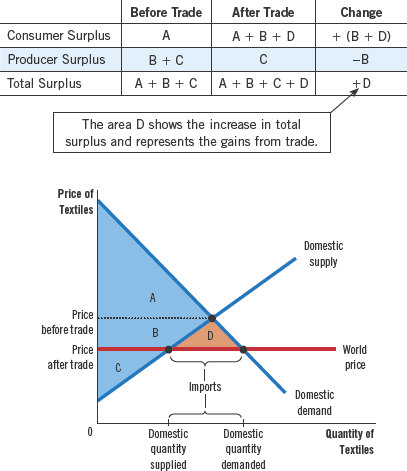

The Gains and Losses of the an Importing Country#

When a country allows trade and becomes an importer of a good, domestic consumers of the good are better off, and domestic producers are worse off.

Trade raises the economic well-being of a nation in the sense that the gains of the winners exceed the losses of the losers.

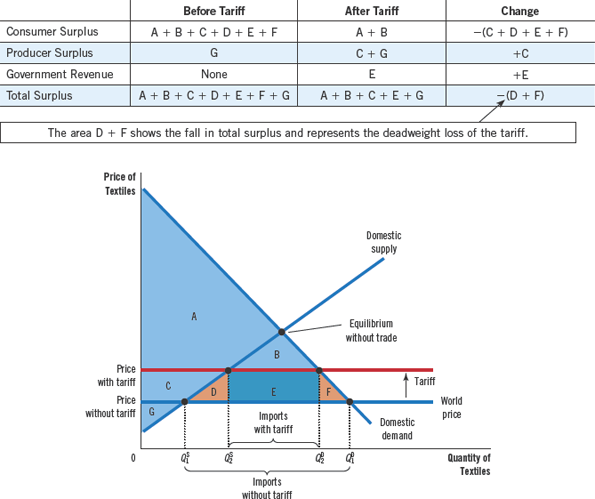

The Effects of a Tariff#

A tariff is a tax on imported goods. A tariff only has an effect on the economy when the good in question is being imported.

A tariff reduces the quantity of imports and moves a market closer to the equilibrium that would exist without trade.

The tariff reduces the quantity of imports and moves the domestic market closer to its equilibrium without trade.

The Lessons for Trade Policy#

Another way of restricting international trade is imposing import quotas, which are much like tariffs. Both tariffs and quotas raise the domestic price of a good, decrease the welfare of domestic consumers, increase the welfare of domestic producers, and cause deadweight losses.

The main difference between import quotas and tariffs is that tariffs raise money for the government and quotas provide surplus for those who obtain permits to import.

Other Benefits of International Trade#

Increased variety of goods

Lower costs through economies of scale

Increased competition

Increased productivity

Enhanced flow of ideas

9.3 - The Arguments for Restricting Trade#

The jobs argument

The national-security argument

The infant-industry argument

The unfair-competition argument

The protection-as-a-bargaining-chip argument